When you walk into a doctor’s office, you expect care-not a financial trap. But for millions of Americans, a routine visit can lead to surprise bills, hidden fees, or even damage to their credit score. In 2024 and 2025, New York State rolled out some of the strongest patient protection laws in the country, targeting exactly these problems. These aren’t vague guidelines-they’re enforceable rules with real penalties. And they’re changing how healthcare providers handle your consent, your money, and your rights.

Separate Consent for Treatment and Payment

For years, patients signed one form at check-in that bundled together consent for treatment and consent to pay. That form might have looked like a standard intake document, but it often trapped people into agreeing to financing plans they didn’t fully understand. Starting October 20, 2024, New York law Public Health Law Section 18-c made that practice illegal. Providers can no longer combine treatment consent with payment consent. They must get your signature on two separate documents.

This change matters because it gives you real control. You can agree to get an MRI without automatically agreeing to pay for it through a third-party financing company. If a provider tries to slip a payment agreement into your treatment consent, they’re breaking the law-and facing a $2,000 fine per violation. The New York State Department of Health made this clear in guidance issued just two days before the law took effect. But here’s the twist: as of August 2025, enforcement of Section 18-c was suspended. That doesn’t mean the law is gone-it means providers are waiting for clearer rules. Until then, you should still ask for separate consent forms. If they refuse, you have grounds to complain.

No More Filling Out Your Financing Applications for You

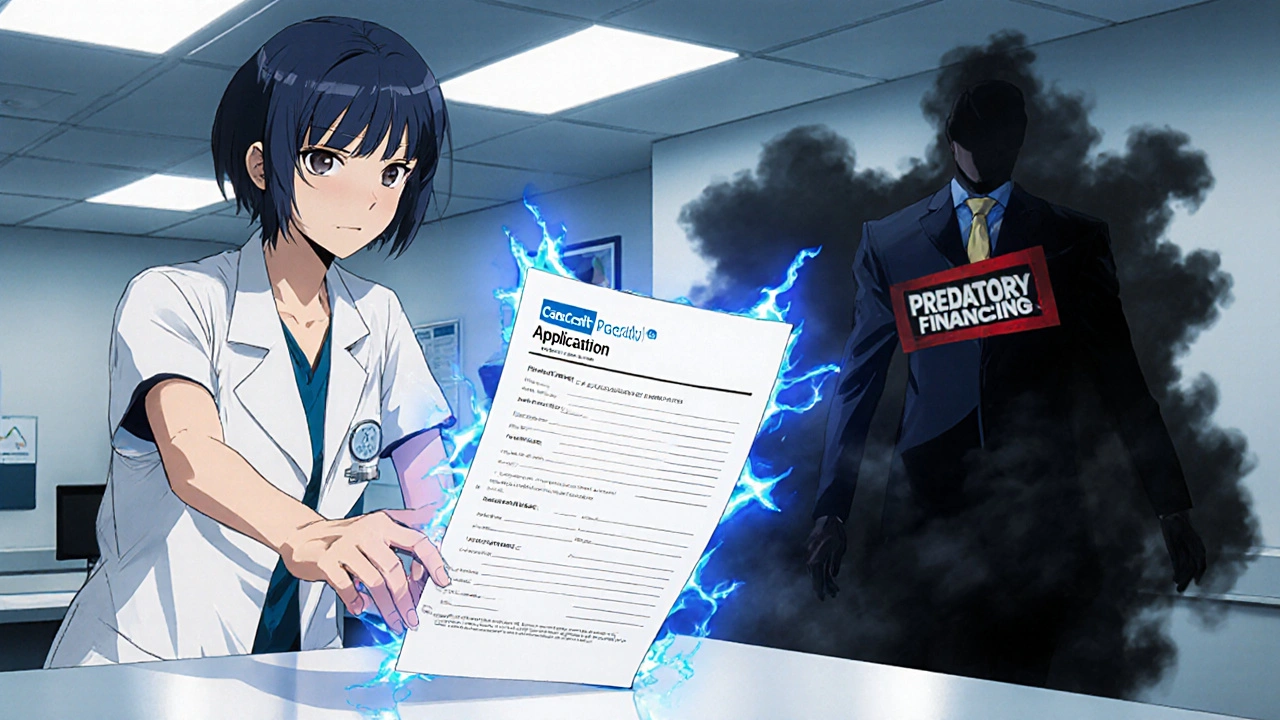

Ever been handed a CareCredit® application at the front desk and told, “Just sign here”? That’s now illegal under General Business Law Section 349-g. Healthcare providers can’t complete any part of a medical financing application-even if they say they’re “just helping.” They can answer your questions. They can explain what CareCredit is. But they can’t fill in your income, your Social Security number, or your signature. The application must be entirely your work.

This law targets predatory sales tactics. Some clinics pushed patients into high-interest medical loans they didn’t need, often without explaining the terms. Now, if a provider even touches your application form, they risk a $5,000 fine per violation. The Department of Health clarified this point: staff can sit with you while you fill it out, but they can’t guide your hand or pre-fill fields. This puts the power back in your hands. If someone tries to help you complete the form, say no. You have the right to do it yourself.

Don’t Let Them Keep Your Credit Card Before Emergency Care

Imagine you’re rushed to the ER after a fall. The staff asks for your credit card before they even check your vitals. That’s not normal-it’s illegal under General Business Law Section 519-a. New York now bans providers from requiring credit card preauthorization or keeping your card on file before giving you emergency or medically necessary care. This includes urgent care centers, outpatient clinics, and even some dental offices.

Why is this important? Because if you pay with a regular credit card, you lose key protections. Medical debt from healthcare-specific financing products (like CareCredit) can’t be reported to credit bureaus under federal rules. But if you use your Visa or Mastercard, that debt can show up on your credit report, trigger wage garnishment, or even lead to liens on your home. Section 519-a forces providers to warn you about this risk every time you use a traditional credit card. They must give you a written notice explaining that your payment method affects your legal protections. If they don’t, you can file a complaint with the state attorney general.

How These Laws Compare to Federal Rules

The federal No Surprises Act, which took effect in January 2022, stops surprise bills from out-of-network providers. That’s a big win-but it doesn’t cover what happens inside your doctor’s office. New York’s laws go further. They tackle in-network financial traps: forced financing applications, combined consent forms, and credit card pressure tactics. While the federal government removed medical debt from credit reports in 2024, New York is making sure you’re not tricked into using credit cards in the first place.

Here’s the key difference: federal law protects you from unexpected bills. New York law protects you from being manipulated into debt. If you’re offered a payment plan, you now have the right to say no-and to know exactly what you’re signing up for. The state is treating medical finances like consumer finances: with clear rules, transparency, and consequences for abuse.

What This Means for You as a Patient

These laws don’t just change paperwork-they change your power. Here’s what you should do:

- Always ask for separate consent forms for treatment and payment. If they give you one form, refuse to sign until you get two.

- If someone tries to help you fill out a CareCredit® or similar application, say, “I’ll do it myself.”

- Never hand over your credit card before you’re treated in an emergency. If they insist, ask for a supervisor or call the state’s health hotline.

- Every time you pay with a credit card, ask for the required risk disclosure. If they don’t give it to you, note the date, time, and provider name.

- Keep copies of all signed forms. If you’re later hit with unexpected debt or a credit report error, these documents are your proof.

You’re not just a patient-you’re a consumer. And like any consumer, you deserve clear terms, no hidden fees, and the right to walk away from bad deals.

What’s Next? Other States Are Watching

New York isn’t alone in this fight. The Consumer Financial Protection Bureau’s 2024 move to remove medical debt from credit reports set a national tone. Experts predict other states will follow New York’s lead. California, Illinois, and Massachusetts are already reviewing similar bills. The trend is clear: medical debt can’t be treated like credit card debt. It’s a health issue, not a financial one.

For now, New York’s laws are the strongest in the country. Even with Section 18-c’s temporary suspension, the other two rules are active and enforceable. If you live in New York, use them. If you live elsewhere, ask your provider: “Do you follow New York’s patient protection rules?” If they don’t know what you’re talking about, it’s time to push for change.

Where to Report Violations

If a provider breaks these rules, don’t stay silent. File a complaint with:

- New York State Department of Health - for issues with consent or billing practices

- New York State Attorney General’s Office - for deceptive or unfair business practices

- Consumer Financial Protection Bureau (CFPB) - for credit reporting issues or financial product abuse

Each agency has an online form. Keep your records. Your voice helps protect others too.

Author

Mike Clayton

As a pharmaceutical expert, I am passionate about researching and developing new medications to improve people's lives. With my extensive knowledge in the field, I enjoy writing articles and sharing insights on various diseases and their treatments. My goal is to educate the public on the importance of understanding the medications they take and how they can contribute to their overall well-being. I am constantly striving to stay up-to-date with the latest advancements in pharmaceuticals and share that knowledge with others. Through my writing, I hope to bridge the gap between science and the general public, making complex topics more accessible and easy to understand.